The last WHC Action Price buy was $5.61 and it reached $11.04 - a gain of 97%.

The ATRTS kicked in today and WHC opened at $8.27 - a gain of 47% on the Action Price.

Wow. That’s a massive 50% less profit from the high that was reached.

Seems quite an extreme drop in profit from the high. Any thoughts.

Yep - the giveback in WHC is horrendous but I don’t know what you can do as the trail stop probably kept the trade alive a bit longer earlier on.

Agree we need these big (5R - 10R) winners to negate the losses though.

If you have ORG in your portfolio that will cheer you up

Must say i was a bit disappointed with the amount that was left on the table with the WHC trade - as they say let the profits run and cut the losses - just feels like the TSL should have been a wee bit tighter to capture a bit more of the profit

Hi All,

What is being commented on here is known as “end of trade drawdown” and is to be expected in any trend following system.

Drawdown when it happens represents pain and our mind instantly reacts by trying to “work out” how we can avoid it next time, raising questions like “What if we used a tighter trailing stop?”

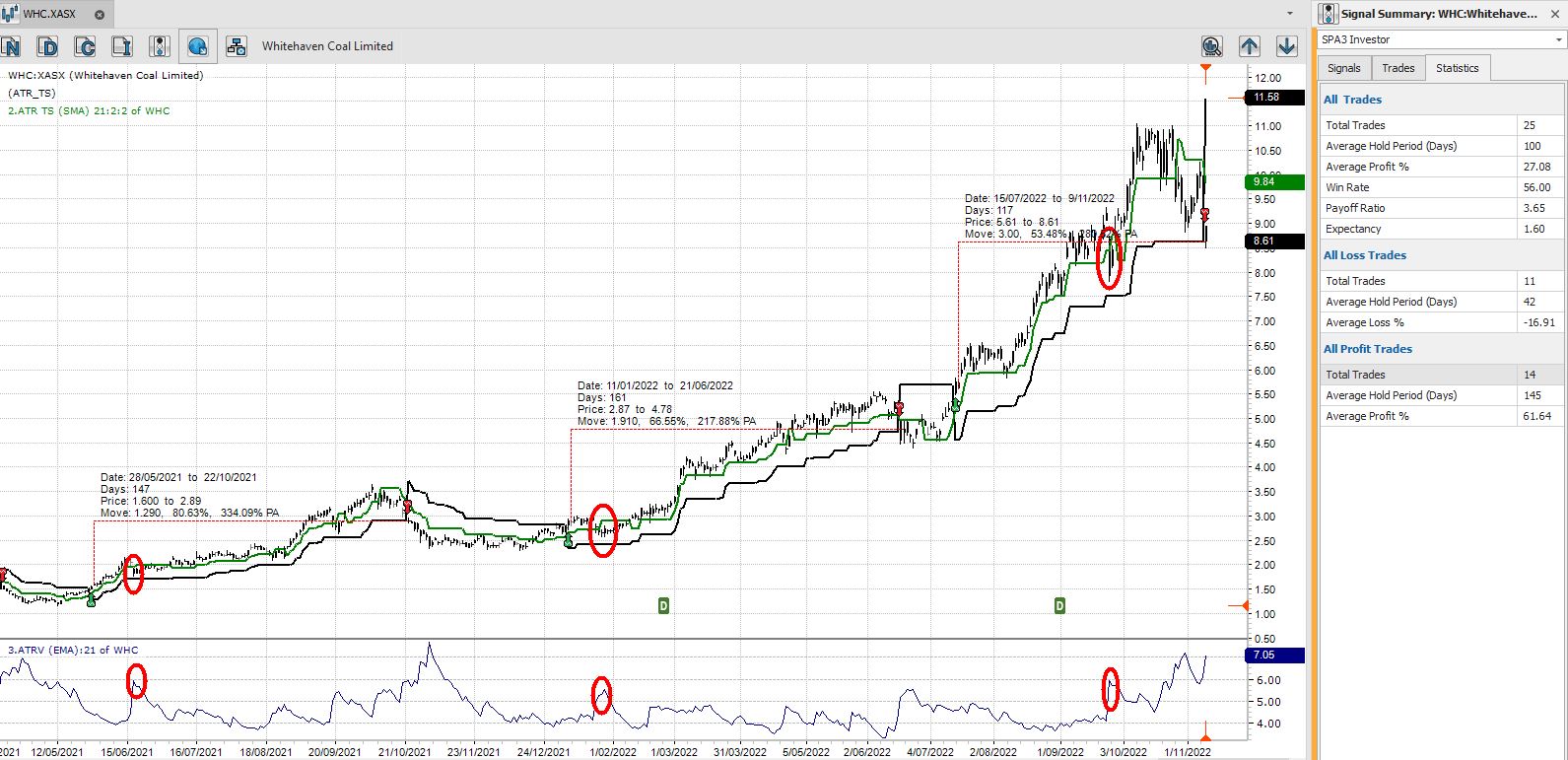

For visual purposes I have attached a very recent example of 3 trades (beware small sample sizes) on WHC to show the impact of using a tighter trailing stop. (Red circles on the chart)

You’ll notice that the SPA3 Investor Trailing stop advances or trails more slowly when the stock volatility (ATRV) shown in the lower panel of the chart increases, giving the stock room to move.

If the trailing stop were to hug the price closer then exit signals would be produced much sooner.

In two examples using a tighter trailing stop would have meant exiting early and missing out on the substantial gains that the “looser but dynamic” trailing stop of SPA3 Investor produced.

But 3 trades is still not a sufficiently large sample size on which to base an idea, it’s just too small. So we need to take a much bigger sample size to see what we can learn.

The statistics of the SPA3 Method clearly show an Edge when executed over the larger time frame and have been included in the image above.

At our forthcoming Connect & Grow live events Gary will be discussing the research that he has been performing over the last 4 months, with a view to reducing portfolio drawdown. There’s some great outcomes from this, but it will still require a specific mindset for long term success.

There are many potential reasons why one might place so much emphasis on a single trade but it all comes back to Psychology and becoming a “peaceful investor”. Here’s a link to Gary’s session on the 5 Key skills that will help you to do that.

No doubt being able to answer some “what ifs” along the way helps, and our SPA3 Investor Trade Simulator will help you to do this in the next release.

We’ll be demonstrating this at the C&G live events in readiness for your explorations so please keep an eye out for the invitation.

Hard to make a buck unless you are in resources. I have CSL WBC CBA NAB MND SEK CPU WES so suffering from selection bias currently

Just catching up on this after focusing on some other research work. Some points to add to the discussion.

- A closer trailing stop will just make the system a shorter term system. It doesn’t eradicate ETD (End of Trade Drawdown, just makes it feel like less. But introduces other occurrences which will also be seen as issues my some (maybe most), like breaking what are now one longer profit trade into 2 or 3 shorter trades with at least one, maybe two being loss trades.

This in turn changes the expectancy, avg hold period of trades, frequency of trading, time and effort to manage a portfolio… it makes it a different system.

- As Dave points out, this discussion is based on a sample of 1. Beware the sample of 1, 2 or a few. If I was paid a dollar for every time I’ve said or written that over the last 24 years…

For every sample of 1 anybody bases an hypothesis on, I’ll find my sample of 1 (actually many more) to prove the exact opposite of the points they make on their sample of 1.

That’s why Expectancy is only meaningful over a large enough sample. Some statisticians say a minimum of 30 in a sample is statistically significant on which to base decisions. The higher the better. There will always be exceptions. Should decisions be made on exceptions and outliers alone?

That’s why we research and decide on criteria that are measured over a large sample of trades over many different types of market conditions.

- To conclude, how is the ATR trailing stop supposed to work? Well, in many other cases, volatility is maintained or decreases as a trade matures, which brings the ATR TSL closer to price action and reduces ETD.

The top 3 largest profit trades in the ASX Public Portfolio all maintained their volatility as measured by the ATRVE at each end of the trade. You can research more to help get a more balanced view.

In this case with WHC, volatility bottomed at 3.62 then advanced to 7.05 on the exit signal. Meaning, this sample of 1 does not describe a typical end of trade.