Just a thought about this exit in SPA3 Income, I notice we’ve had 2 such exits since the start of the system ( both profits and AGQ a phenomenal result!) and I am wondering if, given the nature of the signal- which follows a strong run up, that a MOO order might work better than MOC for this signal, so that you are more likely to capture the effect of the euphoria before it subsides, which it is likely to do.

Obviously 2 only examples so would need to be thoroughly back tested but seems logical to me given the specific nature of this signal.

Any thoughts Gary or David?

Wakefield,

You can scan a bunch of historical signals to get a bigger sample and form a view.

Gary, I haven’t been able to work out how to do that

I went manually through a 5 year Simulation I had done and couldn’t see it made much difference so maybe nothing in it?

If someone could do the scan I would like to see it

thanks

Wakefield,

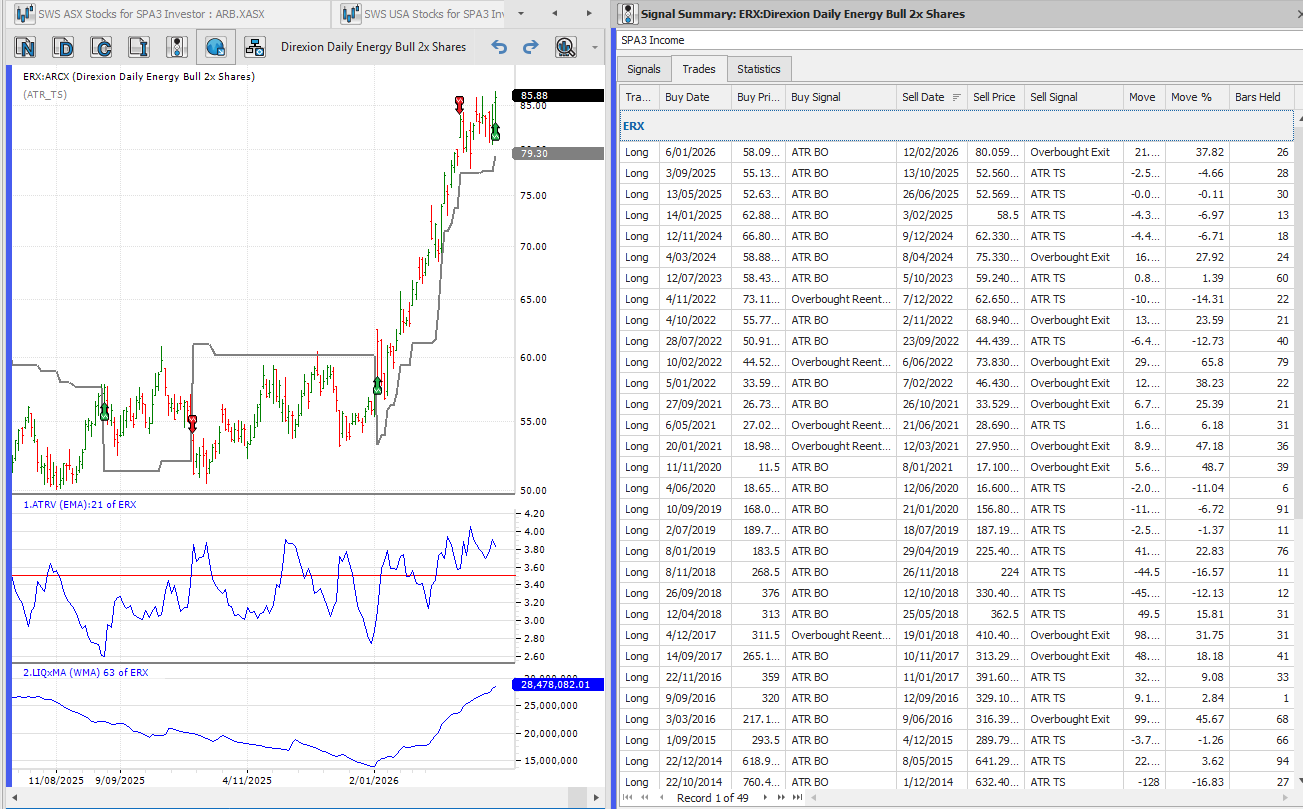

No need to run a Scan. This is ‘automatically’ done for you when using Signals Summary:

All the signals are listed in date order under the Trades tab on the right. You can double click on the individual trade in the ‘trades database’ and BC will take the chart to that signal and date in the chart on the left.

You can eyeball these in all the ETFs in the Universe. You also Export all the trades for each ETF or just the OverBought Exits and Re-entries into a spreadsheet for the entire Universe if you want.

That way you can form a view about the MOO vs MOC and any other views.

Exercises such as this help build trust in an “edge”, which is important to be able to build the skill of “thinking in probabilities” at all, let alone with this specific “edge”. The odds of becoming a consistently successful and peaceful trader are very slim without truly learnng to “think in probabilities”.

thanks Gary I’m into it!